Swift Transportation promises ‘enhanced’ driver pay as shortage crimps growth

William B. Cassidy, Senior Editor | Jul 25, 2014 3:09PM EDT

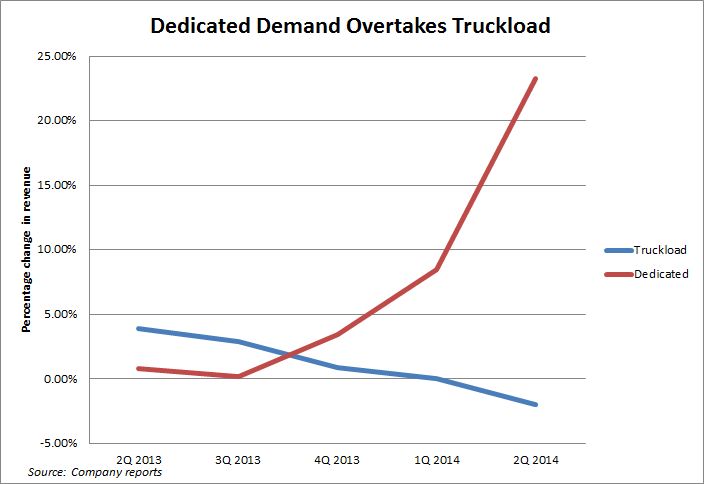

Year-over-year percentage changes in revenue, excluding fuel surcharges, for Swift’s truckload and dedicated divisions are following divergent paths.

Swift Transportation, the largest U.S. truckload operator, got even bigger in the second quarter, but potential growth was restrained, the company said, by a “challenging driver market.”

“Our driver turnover and unseated truck count were higher than anticipated,” Swift said in a letter to shareholders. In reaction, the company sold trucks to offset the impact of idle equipment.

“We believe the best investment we can make at this time, for all our stakeholders, is in our drivers,” the company said. “Our goal is to clear the path for our drivers by helping them overcome challenges, eliminate wait times and take home more money. We believe we can accomplish this through improved productivity and enhanced pay packages.”

Swift’s difficulty finding drivers in the second quarter signals the shortage of available drivers will be the leading check on over-the-road truckload capacity this peak shipping season. The company is one of the largest employers in trucking, with about 14,700 drivers and 19,600 employees at the end of 2013. Swift also has contracts with more than 5,000 owner-operators.

The so-called driver shortage is a roadblock to expansion, limiting incremental growth in truck capacity, and a prime reason truck rates are rising at a faster pace in 2014. The number of heavy truck or tractor-trailer drivers increased 1.9 percent in 2013, after rising 3.2 percent in 2012 and 2.9 percent in 2011, according to the U.S. Bureau of Labor Statistics. The number of drivers fell 13.4 percent from 2007 to 2010 and has risen only 8.1 percent since.

Increasingly, truckload carriers are caught in a Catch 22-like situation: They need more drivers to increase revenue, but the cost of those drivers is eating into profit margins and limiting their ability to hire more drivers. The likely solution will entail even higher truckload rates.

In its shareholder letter, Swift said rate increases will likely hit the 4 to 5 percent range this fall. Higher pricing supported a 3.7 percent increase in revenue per loaded mile, excluding fuel surcharges, in the second quarter, and pricing momentum is growing, the company said.

Even so, Swift is bracing for cost headwinds in the second half of 2014 as it tests and implements several driver initiatives. “The investment in our drivers will be more immediate and the benefits are expected to be derived over time,” the truckload carrier said. “We believe by making these investments now, we can deliver on our goals for 2015 and beyond.”

Overall, Swift’s total revenue rose 4.5 percent year-over-year to $1.08 billion, and 6.7 percent from the first quarter. But two out of four divisions reported lower revenue than a year ago, and three reported lower profits, including an operating loss at Swift’s intermodal division. The company’s net profit declined 19.4 percent from a year ago to $40.2 million as operating expenses rose 5.7 percent. Salaries, wages and benefit costs rose 6.3 percent.

Swift’s truckload revenue — which accounts for about 53 percent of the $3 billion company’s total revenue — actually shrank 2 percent year-over-year in the quarter to $459.1 million, excluding fuel surcharges, partly because Swift shifted some truckload resources to its dedicated division. Truckload profit, however, rose 7.7 percent to $69.6 million.

The dedicated business grew 22.1 percent, with revenue sans surcharges rising 23.1 percent in the quarter to $183.3 million. “We have seen a dramatic increase in demand for our dedicated service offering over the past six to nine months, which has led to strong growth, but the associated start-up costs have placed short-term pressure on margins,” Swift said. Also, although more drivers are attracted to dedicated work, which is often short-haul in distance, allowing for regular home time, dedicated driver pay per mile is higher, Swift said.

The dedicated division’s adjusted operating profit dropped 13 percent to $21.1 million.

Lack of drivers also crimped revenue at Swift’s Central Refrigerated segment, which saw revenue excluding surcharges drop 1.3 percent to $86 million and its operating profit drop 35.3 percent to $3.7 million. The refrigerated business, acquired by Swift last August, also fielded fewer trucks, and had higher costs due to ongoing systems integration with Swift.

Swift increased intermodal revenue, excluding surcharges, 11.9 percent to $80.8 million, driven by a 10.9 percent increase in loads. But the intermodal unit lost $495,000, compared with a $788,000 operating profit a year ago. The division is expected to get back on track as Swift expands its fleet of domestic intermodal containers, adding 500 containers in the late third quarter. “These new containers are expected to drive further revenue growth and improve margins as we drive efficiency in our operating assets and better absorb our fixed costs,” Swift said.

Contact William B. Cassidy at wcassidy@joc.com and follow him on Twitter: @wbcassidy_joc.

{kind=link}